A critical analysis of green neo-banks: greenwashing or effective leverage?

Emilie Combres

Chargée de communication

Temps de lecture : 15 minutes

The new Banking on Climate Chaos report has just been published, and the figures are alarming. This analysis, carried out by several international organisations, takes stock of the financing provided by the world’s largest banks to fossil fuels. With the latest IPCC report recommending a 3 to 6-fold increase in funding for the ecological transition, we might expect banks to gradually disinvest from polluting sectors. On the whole, this has been the trend over the last few years, even though financing for fossil fuels is still too high, but 2024 is even more disappointing: the world’s 65 largest banks allocated $869 billion to fossil fuels, 23% more than in 2023. In total, 7,900 billion dollars have been invested in this ultra-polluting sector since the Paris agreements, which warned of the problem. French banks are not to be outdone: in sixth place, they have invested more than 20 billion euros in the sector this year. As a result, bank investments are becoming a growing concern in France, and initiatives have been developed to try and respond to this: the ‘green’ neo-banks. You’ve probably already heard of them, with Helios or Green-Got for example, and you may also have calculated your bank’s carbon impact and changed bank accordingly. But what is the reality? Are these new banks really “green”? Does changing bank really have an impact on our CO2 emissions? That’s what we’re going to try to answer in this article.

More and more carbon footprint calculators for banks are appearing, either from external organisations (Oxfam, Rift by ADEME, etc.) or from the banks themselves, particularly the green neo-banks, which promise a significantly lower footprint by moving our accounts to them. In reality, it is very difficult (if not impossible) to calculate the carbon footprint of your bank account and therefore to give concrete figures that make sense. Nevertheless, we are going to try to assess what impact these green neo-banks may have. But first of all, it’s important to remember that these ‘neo-banks’ are not banks in the strict sense of the term, but payment service agents, administratively affiliated to traditional banks. For example, Green-Got is an agent affiliated to Crédit Mutuel Arkea, and Helios to Okali (a Crédit Agricole subsidiary), but its deposits are also with Crédit Mutuel Arkea.

We can already ask ourselves whether these ‘neo-banks’ are more environmentally friendly than Crédit Mutuel, and if so, in what way. Helios and Green-Got promise to reduce their emissions:

- Not to invest your money in fossil fuels

- Invest your savings in ecological transition projects

- Donate to environmental charities

So we’re going to look at the effectiveness of each of these three strategies.

Divestment: a symbolic but insignificant gesture in the current system

The first argument put forward by these “green banks” is that they do not finance sectors that are harmful to the environment, such as fossil fuels. For example, Helios writes in its 2024 impact report that it has divested more than €600 million from “big polluting banks”, money that now emits 79% less CO2, having avoided 320,000 tonnes of CO2 since its creation. However, the impact of divestment is not equal to the carbon impact of the investment: under the current system, divested funds can be quickly replaced by other investors, which limits the direct effect on the behaviour of companies and their CO2 emissions. “If the French banks don’t want to, we’ll find another bank, the world is a big place, there are lots of American and Japanese banks […] It’s a good business and when you have a good business, you find bankers” says the CEO of Total Energies himself.

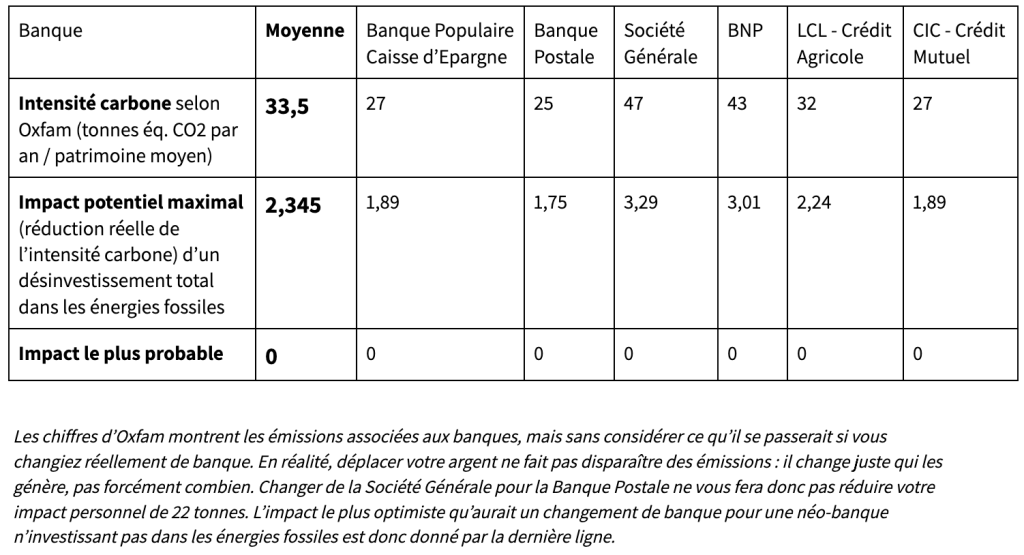

Unfortunately, the science bears this out: most studies on the impact of divesting from fossil fuels (review of several dozen articles by Platinga et al, ESG Funds & Climate Impact study by Giving Green, study by Oxford University researchers Ansar et al) have found no significant effect in terms of reducing CO2 emissions. This can be explained by a number of factors, including the fact that fossil fuel companies remain profitable despite divestments, allowing other investors to step in and continue financing these industries. Companies can also adjust their financial strategies to offset the impact of divestment, which limits its effect on their emissions. However, some more optimistic studies (Marupanthorn et al) estimate that divestment from the energy and utilities sectors can lead to an effective reduction in carbon footprint of up to 7%, a percentage well below the orders of magnitude evoked by green neo-banks or Oxfam. This reduction would be achieved mainly by reallocating funds to less carbon-intensive sectors and by adjusting portfolios according to ESG criteria (the framework used to measure a company’s non-financial performance in terms of the environment, society and governance). So, in the most optimistic case (i.e. 7% reduction in emissions) and using the average financial wealth of the French as a benchmark (€72,380 according to the Allianz 2024 Global Wealth Report), switching to a green bank could save each French person around 2.3 tonnes of CO2 out of a total of 33.5 (average CO2 equivalent of €7,280 from 6 major French banks, calculated by the Oxfam simulator), an impact similar to that of adopting a vegan diet.

As a reminder :

- The figure of 7% is still a long way from the 79% reduction in emissions claimed by Helios.

- The majority of studies do not support this (0 tonnes less according to the 3 other articles studied).

- Carrying out a carbon audit of your bank account makes little sense in reality because of the complexity of the banking system (the independent media Bon Pote has also produced an article on this subject).

It might be thought that the money we deposit in a bank does, in fact, have an impact in the sense that it gives liquidity to the chosen bank, enabling it to lend more or less to polluting companies. However, the link is not direct (and the leverage relatively ineffective as a result) because in the case of loans, money is created ex nihilo (i.e. by a game of writing, but it is not money that actually exists). Even in the unlikely event of a major bank going bankrupt as a result of a massive boycott, another bank would take over and continue to invest in polluting sectors in its place, as explained above. The Giving Green study suggests that funds with a strong shareholder commitment, which retain shares in fossil fuel companies but exert pressure via shareholder resolutions or votes, achieve more measurable results (by voting against the implementation of a particularly destructive project, for example).

The disinvestment in fossil fuels promoted by the ‘green’ neo-banks therefore appears to be relatively ineffective on its own. But if a bank’s money is divested from one sector, it is invested in others. It is these investments in more sustainable sectors that we are now going to look at.

Investment via our savings: between inefficiency and constraints

Over the last 18 months, Green-Got claims to have invested €55 million in environmental transition sectors. Helios puts the figure at €10 million. For investments to have a real positive impact, they must stand out from the crowd and meet certain criteria:

- Investing in underfunded sectors, where the absence of investment creates a real opportunity for impact.

- Accepting lower financial returns to enable greater social impact.

- Focus on neglected issues that offer great potential to make a unique contribution.

- Leveraging an information or network advantage to identify opportunities that others might overlook.

These criteria are not highlighted in GreenGot’s methodology, which suggests that they may not be using the best methods to have the greatest impact and that their investments do not necessarily have a marginal impact. Although the green neo-banks support some interesting initiatives, it is difficult to guarantee that all their projects have a strong social and environmental impact. For example, some of the green investments they make are in sectors that are already relatively mature, such as solar energy. Investments in fields that are still emerging, such as super-heated rock geothermal energy (a project supported by the Clean Air Task Force and particularly recognised for its effectiveness), guarantee a greater impact, aiming to recreate the same tipping point that occurred with solar and wind power. As another example, GreenGot’s home page highlights sectors with contested benefits, such as Agronutris, with its insect farming business (which is in safeguard proceedings). In particular, they explain that insect production emits 100 times less CO₂ than meat… except that Agronutris doesn ‘t sell a meat substitute. Given the very low consumer acceptability of insects, they make animal feed. And because insects need a lot of energy to heat, their emissions are up to two to ten times higher than the food they are trying to replace, according to this article from theNational Insect Farming Observatory.

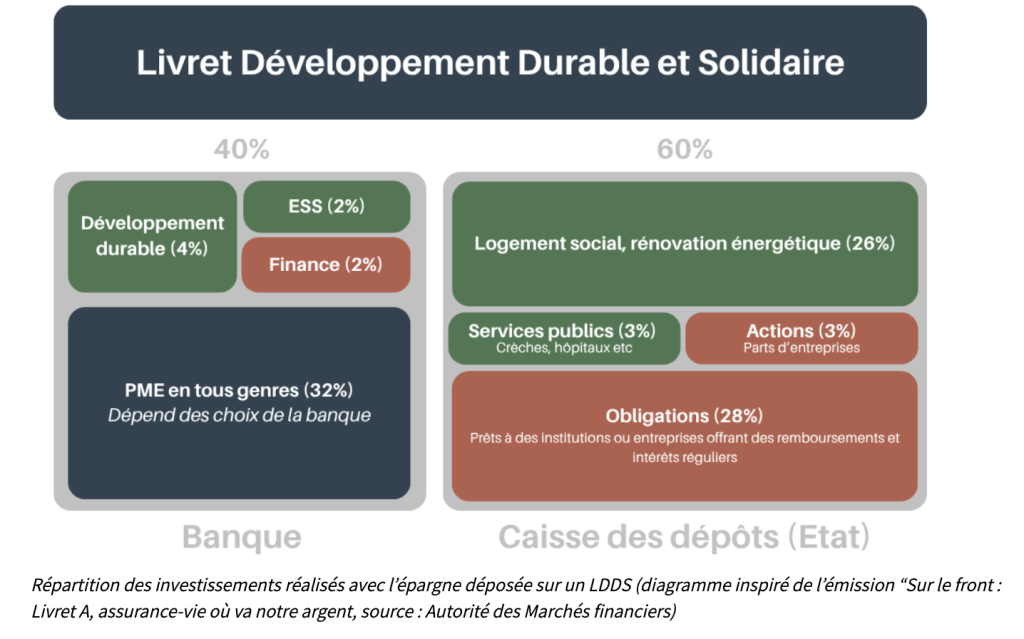

Aside from the questionable effectiveness of the projects in which some neo-banks invest their money (well, ours), there is another important point to be made. The investments are made using our savings (Livret A, LDDS, PEL, LEP, life insurance, etc.) and not our current account. As Green-Got themselves say: “At Green-Got, funds from payment accounts are blocked in ring-fenced accounts, so they cannot be used to invest in the economy, either for Arkéa or for Green-Got. These funds are said to be disinvested”. However, the best-known savings books (Livret A, Livret Développement Durable et Solidaire (LDDS), Livret d’Epargne Populaire (LEP), etc) are regulated by the State and partially earmarked for compulsory funds, 60% of which go to Caisse des Dépôts. The problem is that this public institution itself invests at least €9.2 billion ofthe €323 billion at its disposal in companies involved in fossil fuels (a figure that is largely underestimated). For an LDDS passbook account, for example, the estimated breakdown of investments is as follows:

So, for this type of savings account, even in a bank that claims to be eco-responsible (a neo-bank or a more traditional bank such as Nef, Crédit Coopératif, or even Banque Postale or Crédit Mutuel, which have recently made commitments regarding savings investments), 30% of your money will not necessarily be invested in environmental or social projects. On the other hand, whichever bank you choose, at least 40% will be used to finance virtuous projects.

Other types of savings are essentially life insurance accounts, which allow you to invest your money in funds. Here again, your bank is nothing more than an intermediary that charges more or less to invest on your behalf in the sectors it chooses. A green neo-bank will logically invest in more sustainable sectors, but they are not the only ones. There are now labels for investment funds, such as the SRI (Socially Responsible Investment)label, set up by the French Ministry for Ecological Transition and Solidarity, whose criteria have recently been updated to ensure that these funds respect a number of binding and ambitious commitments in terms of environmental and social policy. More and more traditional banks and insurance companies are offering their customers the chance to invest in these funds. Some cooperative banks (La Nef and Crédit Coopératif, for example) also offer their customers member status and voting rights, giving them a direct say in the choice of projects supported. It may therefore be worth investigating several of these banks, and comparing their management fees with those of green new banks, which are sometimes higher.

When it comes to generosity, why go through an intermediary?

Indeed, the fees charged by these new green banks, whether for savings or current accounts, are often a little higher than average because of their supposedly stronger commitments and lower returns (a marketing argument which, as we have seen, needs to be qualified). In addition to the initiatives mentioned above, they also sometimes give generously to environmentally or socially committed associations, by donating part of their profits to them. Green-Got, for example, claims to have donated 1.1 million euros. At first sight, that seems rather substantial. But let’s do a quick calculation, taking only current accounts into account:

- Green-Got’s first current account offer starts at €6.9 per month, whereas some online banks offer free current accounts. In one year, you could therefore save €82, which you could then donate to high-impact associations and thus avoid up to 82 tonnes of CO2 per year (much more than the 2 tonnes mentioned in the first part of this article).

- Green-Got has around 70,000 customers. If all these customers were to do as described above, this would represent €5.74 million that could be donated each year to effective charities, more than 5 times what Green-Got has donated since it was founded (and not necessarily to high-impact charities).

We can also do a similar calculation with Helios, with their €4 offer and 40,000 customers, and avoid 1.92 million tonnes of CO2 each year by giving to highly effective associations, which is 6 times more than the 320,000 tonnes avoided since their creation according to their impact report.

So, having looked in a little more detail at the main initiatives put forward by the green neo-banks, we feel it is important not to regard them as the best use of one’s money to make a positive impact. Although some of their commitments appear to be greater than those of certain ‘traditional’ banks, they are still far from the effectiveness of more established interventions. Although the emergence of green neo-banks shows a growing concern for socio-environmental issues, individuals can have a greater impact by supporting initiatives that have already proved their effectiveness. This support can also, of course, complement a change of bank, to a green neo-bank, a cooperative bank, or a labelled bank, a change that would certainly be more symbolic than effective in the current banking system.

The difficulty of tackling climate change requires transformative action, and supporting the most effective associations makes this possible.

Tags : English Article