Charities donations and tax: understanding the real impact of tax reductions

Emilie Combres

Communications Officer

Reading time: 10 minutes

At Mieux Donner, we recommend effective charities that fund initiatives with a real impact. In addition to the effectiveness criteria assessed by independent research teams, we also ensure that these charities are eligible for tax relief in France, so that you can make an even greater impact!

Tax relief and charities donations: a double-edged good deed?

In France, individuals can deduct a large proportion of their donations to charitable organisations from their tax bill: 66% of the amount donated in most cases, and 75% in the case of organisations that help people in difficulty. This mechanism, used by around 13% of French households (5.2 million out of 39.9 million), sometimes gives rise to misgivings. Is it fair to take advantage of it? Does this tax lever weaken the funding of public services? Is it an effective way of better directing available resources? Does it encourage an insidious privatisation of the general interest?

We are sometimes asked all these questions, and this article aims to shed some light on the subject. Through this analysis based on historical and international data, the aim is to understand the real effects of this scheme, both for you who donate, and for the associations and the community as a whole.

An old measure, assumed, and specific to France

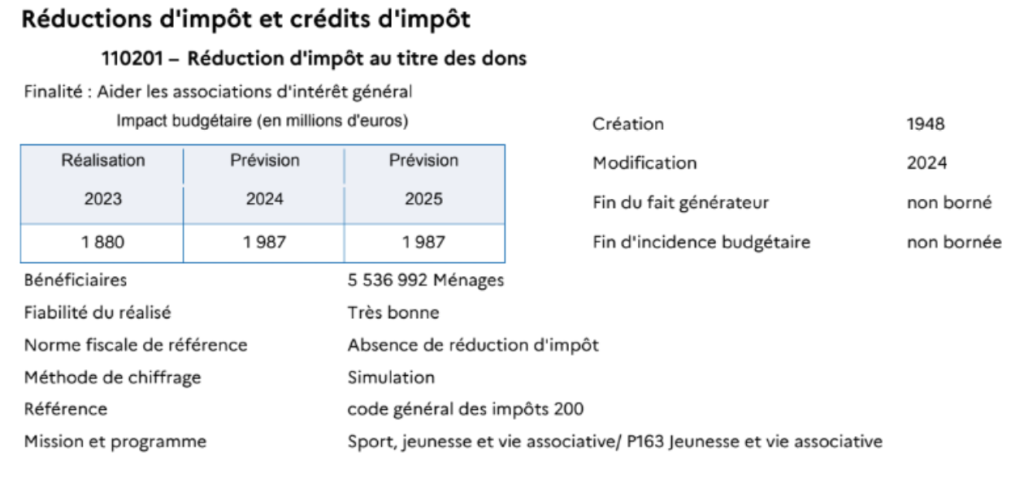

The principle of tax relief for donations is not new: it was introduced in 1948, with a deduction initially set at 25% of the donation. In response to the growing needs of charities, this rate was gradually increased, reaching 50% in 1983, then 66% in 2005 for charities of general interest, and 75% in 2006 for charities listed by the State as helping people in difficulty, up to a limit of €1,000 (ceiling re-evaluated each year). 1

Each year, Parliament votes in the Finance Bill (PLF) to renew this measure. It is therefore far from being a discretionary tax niche: it is an accepted budgetary tool, explicitly integrated into the State’s tax strategy.

Internationally, France stands out. According to an OECD report (Taxation and Philanthropy, 2020), while almost all OECD countries offer some form of tax deduction for donations, few go as far as France in terms of rates or the scope of eligible organisations. By way of comparison:

- In Italy, the tax reduction is 30% of the amount of the donation (increased to 35% for certain NGOs), up to a limit of €30,000.

- In the United Kingdom, the Gift Aidsystem allows a charity to add 25% to a donation (paid for by the government), and high-income taxpayers can deduct an additional amount depending on their tax bracket.

- In Germany, the United States or Belgium, for example, the amount is deducted from taxable income, so the tax advantage varies according to tax bracket, and rarely exceeds 50%.

In other words, few countries offer both such a high rate and such wide access to this reduction as France.

Yet, paradoxically, in France, we remain less inclined to make donations, despite this incentive. According to a report by the Charities Aid Foundation (2016), household donations represented around :

- 0.11% of GDP in France,

- 0.54% in the United Kingdom

- 1.44% in the United States.

This discrepancy can be explained in part by cultural factors (relationship to tax, confidence in associations, philanthropic tradition), but it also raises questions: even a very attractive tax system is not enough on its own to get donations off the ground.

This background is essential if we are to understand how this scheme has become a structuring element of French tax policy. However, in the current context of budget cuts, this measure is being called into question, both by politicians and by taxpayers who fear that it will take away from public services.

What is the real cost to public finances?

The question is often asked: is this mechanism costing the State too much? The PLF 2025 (Ways and Means – Volume II) provides a precise answer: the tax reduction for donations was worth 1.9 billion in 2023, and 2 billion is forecast for 2024 and 2025.

In terms of the overall State budget (around €445 billion in 2025), this corresponds to around 0.4%. In fact, this expenditure ranks 8th out of the 9 main tax expenditures listed by the Ministry of the Economy.

| Order | Measurement number | Measure | Figures for 2025 (in millions of euros) |

|---|---|---|---|

| 1 | 200302 | Research tax credit | 7 745 |

| 2 | 110246 | Tax credit for employing an employee in the home | 6 856 |

| 3 | 120401 | 10% allowance on pensions (including alimony) and retirement pensions | 4 956 |

| 4 | 120108 | Exemption for sums paid (profit-sharing, incentive schemes, matching contributions or capital gains sharing) to employee savings plans and collective or compulsory company pension savings plans | 2 750 |

| 5 | 730213 | 10% rate for improvements, conversions, fittings and maintenance (excluding energy renovation at 5.5%). Article 278-0 bis A, housing completed more than 2 years ago | 2 280 |

| 6 | 730221 | 10% rate for commercial catering (on-site and takeaway, immediate consumption) | 2 123 |

| 7 | 710103 | Level of rates in Guadeloupe, Martinique & La Réunion (8.5% standard rate, 2.1% reduced rate) | 2 060 |

| 8 | 110201 | Tax reduction for donations | 1 987 |

| 9 | 130201 | Deduction of expenditure on repairs and improvements | 1 836 |

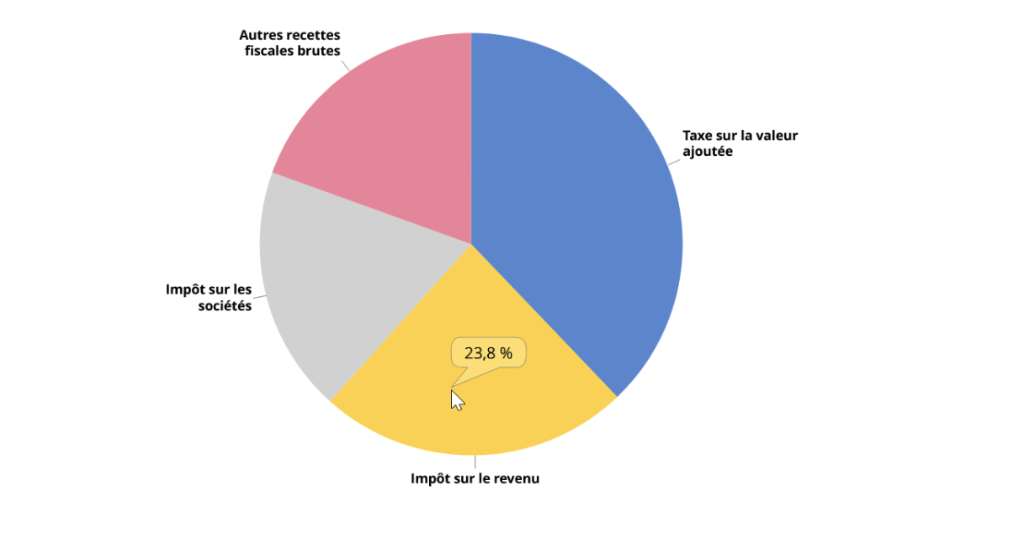

Furthermore, the importance of income tax in government revenue needs to be put into perspective. According to INSEE figures, income tax will account for 106.9 billion euros in 2023, or around a quarter of total revenue. VAT alone generates more than €170 billion, or almost 38 % of public resources. In other words, even a taxpayer who reduces his or her income tax to zero continues to finance public services, in particular through consumption. 2

Finally, it is important to note that the scheme is capped at 20% of taxable income or the amount of your income tax. For donations to organisations helping people in difficulty,the rate is 75% up to a limit of €1,000 in 2025, then 66% thereafter , so even in the event of a sharp rise in donations, the effect on the budget would be contained.

Why maintain this tax system?

The use of tax incentives is based on the principle of directing a proportion of private resources towards causes deemed to be in the general interest. The aim is toencourage more people to donate, and to donate more, even if several studies show that the elasticity of giving (i.e. the impact on the increase in the amount donated) is low, particularly in modest households. However, this may be enough to encourage some people to take the plunge and make a donation, or to increase the amount they donate. For example, if someone wants to donate €100 to a charity, they can give €300 and after tax reduction, it will only cost them €102. In this way, charities can collect three times more than they would have initially, and have three times the impact.

In return, these donations are used to fund initiatives in areas where the state is sometimes absent or ineffective: access to healthcare in poor countries, prevention of existential risks, animal welfare, help for the homeless, support for mental health, and so on. The associative fabric is not just a complement, it is often a lever for social innovation.

As the OECD points out (section 2.2 of the Taxation and Philanthropyreport ), there are many arguments in favour of tax relief, if it is properly managed and evaluated:

- Mobilising private resources for causes in the public interest, without increasing direct public spending.

- Respecting the freedom of choice of citizens, by allowing them to direct part of their tax contribution.

- Supporting the pluralism of associations, particularly in areas where the State has little presence (international aid, social innovation, mental health, etc.).

A fair measure? What inequalities in access reveal

Some people question the fairness of the system: in 2020, the richest 10% of the population accounted for 30.2% of all tax reductions for donations, compared with 1% for the poorest 10%. This is partly due to the fact that the most affluent give more, but also that more of them are taxable and therefore able to benefit from the measure. 3

Does this mean we should not use this reduction when we are entitled to it? The criticism assumes that the amounts not deducted would automatically be allocated to consensual public services, which is not always the case. In reality, the State also funds contested activities: bullfighting and subsidies to intensive livestock farming via the Common Agricultural Policy, public funding of political parties, etc. It is therefore an illusion to believe that every euro of tax corresponds to socially aligned public spending.

Taking advantage of the scheme also means claiming the right to partially direct tax resources, in compliance with collective rules.

Accountability, transparency and efficiency

Using tax relief is not cheating. Nor is it stealing from the state. It’s making use of a democratically voted system, within a limited framework, that allows you to redirect a small part of your tax to causes you consider important. It means playing a part in funding the general interest, while at the same time giving visibility to your commitment to voluntary work. And it’s also an opportunity to have three times the impact: saving 3 times as many lives, avoiding 3 times as much CO2 emissions, etc.

At Mieux Donner, we believe that it’s not enough to give, you have to give effectively. That’s what makes all the difference. If you have the opportunity to do more, thanks to the tax reduction, you might as well make the most of it… intelligently.

Tags : English Article